What is a Valuation Multiple?

A valuation multiple is a ratio that reflects a company's value in relation to a particular financial metric. Simply put, it is a ratio that is calculated by dividing the market or estimated value of an asset by a specific item on the financial statements. Investors also refer to the multiples approach as multiples analysis or valuation multiples.

The multiples approach is based on the theory that similar assets sell at similar prices. It assumes that the ratios used to compare firms, such as operating margins or cash flows, are the same. This is usually done by referring to a financial ratio, such as the price-to-earnings (P/E) ratio, as the earnings multiple. Typically, these ratios are expressed as multiples rather than as percentages.

The valuation multiple is a useful financial measurement tool for investors since it helps determine a company's value as well as compare a company's valuation with its peer group.

How do investors use the Multiples Approach?

The multiples approach is used by investors to determine the value of a company and the companies that are worth investing in.

For this, they start by identifying similar companies and evaluating their market value.

Next, a multiple is calculated for the comparable companies and then aggregated into a standardised figure using a key statistics measure such as the mean or median.

A value identified as the key multiple among the various companies is applied to the corresponding value of the firm under analysis to estimate its value.

In a nutshell, investors use multiples to find businesses that are undervalued and overvalued relative to their intrinsic value.

The following section contains a simple example of the multiples approach to help you better understand.

Example of the Multiples Approach

Let us take the example of a financial analyst who uses the multiples approach to compare where major banking stocks trade in relation to their earnings.

A simple way to do this is to look at the publicly available P/E ratios for the four largest banking stocks in the US. Below is a table containing the trailing 12-month P/E ratio for the top 4 banks as of April 1, 2021.

|

Bank |

Trailing P/E |

|

Wells Fargo |

95.6 |

|

Citigroup |

15.4 |

|

Bank of America |

20.8 |

|

JP Morgan Chase |

17.2 |

By taking a quick look at the table, the analyst can see that Citigroup is trading at a discount to the other 3 banks in relation to its earnings. It has the lowest price-to-earnings ratio at 15.4.

Wells Fargo, on the other hand, has the highest P/E multiple among banks at 95.6.

Next, the analyst calculates the P/E ratio mean (also known as the average) of the four banking stocks. It is done by adding them together and dividing the result by four.

Thus,

(95.6 + 15.4 + 20.8 + 17.2) / 4 = 37 average P/E ratio

The analyst is able to gain a major insight by analyzing the average P/E ratio. With the multiples approach, he now knows that Bank of America, JP Morgan Chase and Citigroup all trade at a discount to the major bank P/E ratio mean.

Valuation Multiple Components

Since the valuation multiple is essentially a ratio, it consists of two components- a numerator and a denominator.

The numerator contains a valuation metric. It can be either enterprise value or equity value.

The denominator consists of a financial metric. These metrics include revenue, EBITDA, EBIT, etc.

As with any ratio calculation, the represented group in the numerator and denominator must match.

Furthermore, it is also critical to gain a deep understanding of the company and its sector in order to make an informed decision. For instance, a mature industry such as construction is likely to have different valuation multiples than a high growth industry such as technology.

In some cases, industry-specific operating metrics and multiples are also used. In the case of social media companies, daily active users (DAUs) would provide a better forecast of their valuation than the company’s earnings.

And in the transportation industry, EV/EBITDAR is frequently used since rental costs are added back to EBITDA. In the case of unprofitable companies, the EV/Revenue multiple is often used since it's the only meaningful option (e.g. EBIT could be negative for such companies)

What are the different types of Valuation Multiples?

Valuation multiples fall into two categories: enterprise value multiples and equity multiples.

Enterprise value (EV) multiples include the enterprise-value-to-sales ratio (EV/sales), EV/EBIT, and EV/EBITDA.

Equity multiples or market multiples include the price-to-earnings (P/E) ratio, price-earnings to growth (PEG) ratio, price-to-sales (P/S) ratio. In essence, they are ratios between share price and an underlying measure of the company's performance such as earnings, sales or book value.

Enterprise value is the value of the operational business. The enterprise value and enterprise value multiples are independent of capital structure. In fact, enterprise value multiples are often deemed better valuation models than equity multiples since they allow direct comparison between different firms even if they have different capital structures.

Moreover, enterprise valuation multiples are less affected by accounting differences. This is because the denominator is calculated higher up on the income statement.

Equities multiples, on the other hand, can be artificially impacted even if there are no changes in enterprise value. Nevertheless, equity multiples are popular with investors because the details are readily available on the internet and are easier to calculate.

Backward and Forward-looking Multiples

A Backward-looking multiple is a valuation method that portrays a company’s value based upon its past performance. They are the multiples you get by dividing a company's present value by its historical earnings, revenue, or book value. This value is then used to predict, with a certain degree of accuracy, a company’s future earnings and stock performance.

Backward-looking multiples, although proven effective, only provide a look into the past, and are not always effective when applied to all companies.

Forward multiples are calculated based on a company's next twelve months EBITDA or EBIT. They are also popularly known as growth multiples.

Forward-looking multiples are multiples that use future earnings as a basis for determining value. In effect, they are analogous to the more commonly used price to earnings ratio. However, instead of using price as a basis for determining value or earnings, they use a forecasted multiple of a firm's earnings as a basis for determining value.

It is often used to estimate the valuation of high growth companies that expect their future earnings to be better than their last twelve months.

Unlike backwards-looking multiples, forward-looking multiples are in line with the principles of valuation. Particularly, that the value of a company is based on its present cash flow, rather than past profits.

In the next section, we take a look at the commonly used valuation multiples.

Equity multiples or Market Multiples

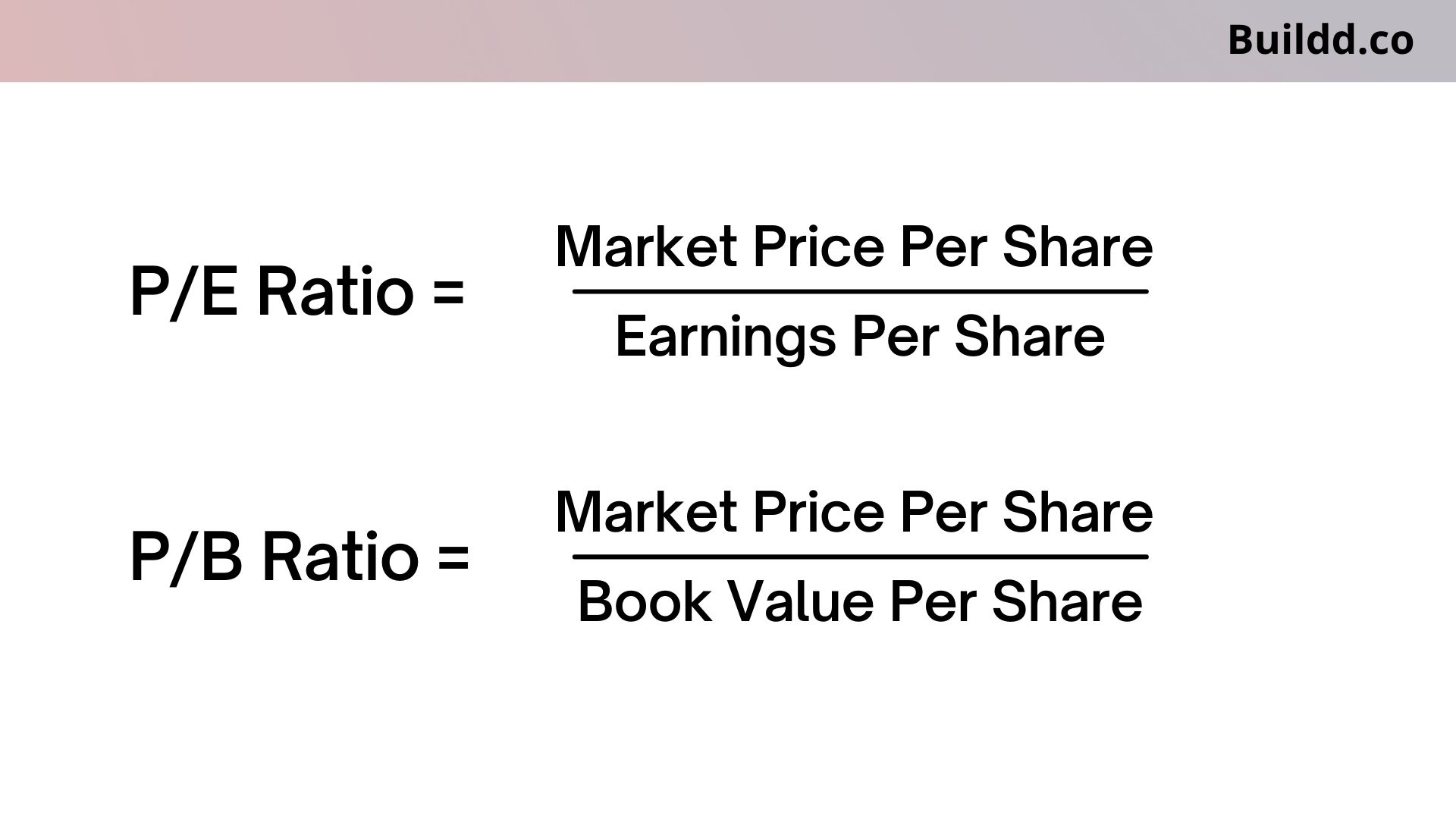

P/E Ratio

P/E ratio (Price-to-earnings ratio) is a way of determining the value of a stock. It's calculated by dividing the current share price by the latest reported earnings per share (EPS). It is one of the most commonly used equity multiples since the data is easily accessible.

Price/Book Ratio

The price to book ratio, or P/B ratio, is a financial ratio that compares the current market price per share to the book value per share of the company's assets. It is often used when assets are used to produce earnings.

Dividend Yield

The dividend yield is the income investors receive for owning shares in a company. The dividend yield is calculated by dividing the dividends per share by the share price.

Simply speaking, it is the amount investors earn for each dollar invested. If the dividend paid by the company is $2.50, and the company is currently trading at $25 per share, then the company's dividend yield is 10%.

Price/Sales

Price/Sales ratio is the ratio of the current price of the stock to its sales (revenue) per share. The calculation is: Price/Sales = Current Share Price ÷ Sales Per Share

Price/Sales ratio is a financial ratio used to value a business based on how much investors are willing to pay for each dollar of sales.

Enterprise value multiples

EV/Revenue

EV/Revenue is a valuation method by dividing enterprise value by yearly revenue or sales.

EV/EBITDA

EV/EBITDA is a valuation metric used to compare the financial strength of companies within the same industry or sector. EV/EBITDA means “enterprise value” (or enterprise value as a multiple of free cash flow) as a multiple of “earnings before interest, taxes, depreciation and amortization.” It is used in place of the P/E ratio since EBITDA doesn't include the value of debt.

The ratio is used to see whether the company's value is overstated or understated. It also helps investors to get a better understanding of the firm's financial position and risk.

EV/Invested Capital

EV is Enterprise value and Invested Capital is the Total Capital. Therefore, EV/Invested Capital is calculated by dividing Enterprise Value (EV) by Invested Capital. It is most popular in industries with high capital expenditures.

Entrepreneurship

Entrepreneurship